How Much House Can I Afford? A Complete Guide to Buying Within Your Budget

Introduction: What “Affordability” Really Means When Buying a Home

One of the first things that comes to mind when you start dreaming about a home is, “How much house can I afford?” It’s a simple question, but it’s one of the most important financial decisions you’ll ever make. It’s not enough to just find a home that looks nice or meets your needs when you buy one. You also need to know how much money you have, set realistic goals, and make sure that your dream home doesn’t become a financial burden in the future.

When you say “affordability” when buying a home, you mean more than just being able to pay your mortgage each month. This means knowing how much it will cost to own a home, such as property taxes, homeowner’s insurance, maintenance, utilities, and maybe even HOA fees. A lot of first-time buyers don’t think about these extra costs because they are only interested in how much they can borrow. They don’t think about how much they have to pay every month.

- When you ask, “How much house can I afford” what you’re really asking is, “How much can I borrow without putting my finances in too much trouble?”

- How much can I spend without going broke while still saving for emergencies, retirement, and my own goals?

- How can I keep my finances from stressing me out if my income changes or I have to pay for something I didn’t plan for?

There is no single answer that works for everyone. Your income, debt, savings, credit score, type of loan, and way of life all affect how much a home costs. Lenders use certain formulas to figure out how much money they will lend you, but what they say you “can” borrow may not be as much as you want. How much house can I afford ?

A lender might give you a $400,000 mortgage if your debt-to-income ratio is good enough. You shouldn’t spend that much right away, though. If you want to keep your budget flexible, you might want to buy less than this amount, especially if you plan to start a family, change jobs, or deal with other big financial changes soon.

When you know How much house can I afford, you feel more in control and sure of yourself when you buy one. This keeps you from falling in love with homes that are too expensive for you and helps you focus on homes that really fit your long-term goals and lifestyle. It also gives you more power to negotiate. When you know how much you can spend and have done the math, sellers and agents know you are a serious buyer.

This guide will show you how to figure out exactly how much house you can afford, what factors affect your mortgage affordability, and what you can do to get your finances in order before you buy. When you’re done, you’ll have a clear plan for how to answer the big question: “How much house can I afford?”

How to Calculate How much house can I afford

Once you know what that means, the next step is to learn how to figure out how much house you can afford. It’s not enough to just guess or look at a lender’s pre-approval number to find out how much housing I can afford. To find what fits into your budget, you need to use good financial rules. home affordability calculator

There are many ways to figure out How much house can I afford, but your income, debt-to-income ratio (DTI), and down payment and loan options are the three most important. home affordability calculator. Let’s look at each one more closely.

Calculation Based on Income

you need to figure out how much of your income you can actually spend on housing in order to figure out how much house you can afford. Most financial experts agree that the total cost of housing each month, including the mortgage, property taxes, insurance, and HOA fees, should not be more than 28% to 30% of your gross monthly income.

You should not spend more than $1,800 a month on housing costs if you make $6,000 a month before taxes. This helps you keep track of your money and makes sure you have enough left over for other bills, savings, and fun things you want to do.

Use this simple formula:

Maximum Monthly Housing Cost = Gross Monthly Income × 0.28 (or 0.30)

This guideline can help you figure out a realistic upper limit, but remember that it’s only one part of the puzzle. You still need to think about your other debts and financial goals. home affordability calculator

Debt-to-Income Ratio (DTI)

The amount of home I can buy depends a lot on your DTI ratio. This number helps lenders figure out if To get your DTI, divide your total monthly debt payments (like credit cards, car loans, student loans, and so on) by your gross monthly income.

If you make $6,000 a month and owe $1,200 a month, your DTI is 1200 divided by 6000, which is 0.20 or 20%.

Most lenders prefer a debt-to-income (DTI) ratio below 36%, but depending on your credit score and the type of loan, some may allow it to go as high as 43%. It’s easier to stick to your budget when your DTI is lower, and you’re more likely to get better mortgage rates.

If you want to keep your money in good shape, try to keep your total debt payments, including the new mortgage, below 36% of your income. If you make $6,000 a month, for instance, your total loan payments shouldn’t be more than $2,160. How much house can I afford.

Choices for Down Payment and Loans

The amount of your down payment directly affects How much house can I afford. A bigger down payment means a smaller loan amount, a lower monthly mortgage payment and possibly a lower interest rate.

Most of the time, you need to put down 3% to 20% on a conventional loan.

FHA loans, which are backed by the Federal Housing Administration, need at least 3.5% down, which is good for first-time buyers.You might not need a down payment for VA loans (for veterans and active duty service members) or USDA loans (for rural areas).

If you buy a house for $400,000,

Your mortgage is $320,000 if you put down 20% ($80,000).If you put down 5% ($20,000), the mortgage goes up to $380,000. This means that your monthly payments will be higher and you will pay more interest over time.

A small down payment might make it easier to buy something right away, but a bigger down payment could save you thousands of dollars in interest over the life of the loan.

Also, keep in mind private mortgage insurance (PMI).If your down payment is less than 20%, you will have to pay PMI until you have 20% equity in your home. How much house can I afford.

Bringing It All Together

To put it simply, here’s a simple way to figure out How much house can I afford

To figure out how much you can spend on housing, multiply your gross monthly income by 0.28 to 0.30.

Your total DTI, which includes your mortgage, should be less than 36%. mortgage affordability.

Credit Repair Magic

Key Factors That Affect Home Affordability

Now that you’ve done the math and figured out how much house I can afford, let’s take a closer look at the main things that can make it more or less affordable. Your income and debt are the most important things, but a lot of other things, like your credit score and property taxes, can have a big effect on how much you can afford to buy a home. Knowing these things will help you make better choices and could save you thousands of dollars over the life of your loan. mortgage affordability.

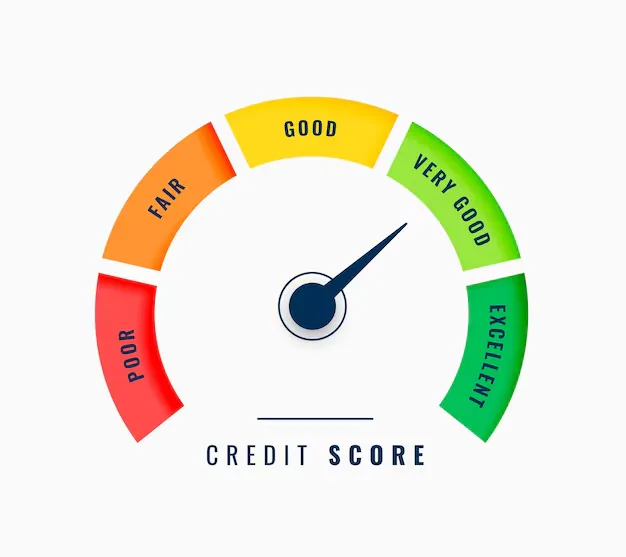

1. Your Credit Score

One of the most important things that affects how much home I can buy is my credit score. This is like your financial report card: it shows lenders how well you’ve handled debt in the past. The better your score, the better mortgage rate you can get. This has a direct effect on how much you can afford to pay each month.

Here’s a basic idea of how credit scores mortgage affordability rates:

- Great (760+): You can get the lowest interest rates available.

- Good (700–759): Prices are a little higher, but they are still very good.

- Affordable (650–699): Can handle moderate interest rates and a small number of loan options.

- People who are poor (under $650) often have trouble getting or qualifying for high-interest loans.

A small change in your credit score can have a big effect. A 1% difference in interest rates on a $300,000 mortgage could mean paying more than $50,000 in interest over 30 years, for example. That’s why paying bills on time, lowering your debt, and checking your credit report for mistakes before applying for a mortgage can help you afford more homes.

2. Interest Rates on Mortgages

The interest rates have a big effect on how much house I can mortgage affordability. If you pay less each month, you can afford a more expensive home with the same monthly budget. On the other hand, when prices go up, your buying power goes down, even if your income stays the same.

For instance:

You can afford a $400,000 home with an interest rate of 3%.

That same monthly payment can only cover a $300,000 home if the interest rate is 7%.

That’s why buying when mortgage affordability are low (or refinancing later when rates go down) can make a big difference in your finances. It’s also a reminder that being able to afford something isn’t just about how much money you make; it’s also about the economy, inflation, and the Federal Reserve’s decisions about interest rates.

3. Length of the loan (15 or 30 years)

The length of the loan is also very important. Most people who buy a home choose between a 15- or 30-year mortgage. Each one affects how much property I can buy in a different way.

A 30-year loan has lower monthly payments, but it costs more in interest over time.

You pay more each month on the 15-year loan, but you save thousands of dollars in interest.

If you want to know how much house I can buy right now, a 30-year term might look good. A 15-year mortgage builds equity faster and helps you get out of debt faster, but only if you can afford to pay more mortgage affordability.

The most important thing is to find a term that works for your finances and your future goals.

4. Taxes on property and insurance for homeowners

Don’t forget about property taxes and homeowner’s insurance, even after you’ve figured out your mortgage. These are costs that I have to pay every year (often included in my monthly mortgage payment), so they can have a big effect on how much house can I afford.

Depending on where you live, property taxes can be very different. For example, a $400,000 house in one county might have an annual tax of $2,000, while the same house in another area might cost $6,000 or more. Homeowners insurance rates also depend on where you live, how old and well-kept your home is, and even how much damage you have done in the past.

When you use an online mortgage affordability calculator or talk to a lender, make sure these costs are included. A lot of first-time buyers forget about them, only to find out later that their total housing costs are much higher than they thought.

5. Other Things That Affect

Your ability to pay can also be mortgage affordability by things like HOA fees, private mortgage insurance (PMI), and even energy costs.If you live in a condo community, the HOA can charge you $200 to $400 a month. PMI can also add 0.5% to 1% to your loan each year. The age and condition of your home can also affect how much you pay each month for utilities and upkeep.

When I’m trying to figure out how much house can I afford, I always have to look beyond the price. Think about all the costs that come up again and again, no matter how small they are. Owning a home is not just about buying it. it is also about keeping it comfortable for years to come.

BUSINESS CREDIT BUILDER

Tools and Calculators

Thanks to cheap online calculators and financial tools, it’s easier than ever to figure out how much house can I afford in the digital age. These tools help you quickly see your budget and make better plans before you talk to a lender or real estate agent. But you need to know what data they use, how they interpret your numbers, and what their results really mean for you in order to use them well.Let’s take it one step at a time.

How to Use an Online Affordability Calculator

The Home Affordability Calculator is a free online tool that helps me figure out How much house can I afford based on my income, debt, down payment, loan term, and interest rate. You can find them on most mortgage and bank websites, and they only take a few minutes to use.This is what you usually have to type in:

Your monthly or yearly income: Include all sources, such as your salary, bonuses, and even freelance work if you do it.

Add up all of your monthly debts, like student loans, car payments, credit card minimums, and any other debts that come up every month.

Down payment or down payment amount: The calculator will show you how the down payment changes the maximum amount you can afford.

The loan term and interest rate help you figure out how much your monthly mortgage payments will be and how much the loan will cost in total. Taxes and insurance on your property: If you’re not sure, Home Affordability Calculator will give you an estimate based on the

Understanding What You Got

When you use a Home Affordability Calculator to figure out how much house can I afford, keep in mind that it is only a suggestion, not a promise. The calculator’s answers are based on common financial ratios and assumptions. How affordable something is in real life depends on how comfortable you are, how you spend your money, and what your lifestyle priorities are.

Here are some smart ways to look at your results

Try to get below the most you can, Just because your calculator says you can buy a $400,000 home doesn’t mean you should. Leave room for savings and options.

Take into account taxes and fees. Your real Mortgage Affordability Calculatory will be lower than what the calculator says if you live in an area with high property taxes or HOA fees.

Do the math again with different situations. Try different down payments, interest rates, or loan terms to see how much can I afford. This helps you get ready for changes in interest rates or a housing market that is very competitive.

Think about what makes you feel comfortable. You might want a smaller mortgage and more money coming in so you can travel or invest. Being able to afford something is not just about math, it is also about finding a balance in your life.

You can see how even small changes affect how much you can buy by playing with different numbers.For example, lowering your interest rate by 0.5% or adding $10,000 to your down payment could make a big difference. How much house can I buy without changing my income? More Tools to Help You Make Your Choice

There are other digital tools that can help you plan better besides cheap calculators:

Calculator for Mortgage Payments, Divide your monthly principal, interest, taxes, and insurance into parts.

- An amortization Mortgage Affordability Calculator will tell you how much interest you will pay on the loan and how long it will take to build equity.

- Apps like Mint or YNAB help you keep track of your spending and get ready to buy a home.

- Credit simulators: These tools, which you can get from the big credit bureaus, show you how things like paying off debt or raising your credit limits can raise your score and make it easier for you to afford things.

- You can get a full picture of your finances by using these tools together. You’ll learn not only how much house you can afford, but also how to pay for it over time.

Budgeting Tips Before Buying a Home

It’s very important to get your finances in order before you sign any mortgage papers. It’s not just about getting a loan approved when you understand how much house you can afford. It’s also about building a strong financial base that will keep you stable in the long run. Your personal budget might tell a different story than what a lender says you can borrow. Smart financial planning, setting aside money for emergencies, and keeping track of all the hidden costs are the keys to being a successful homeowner.

Here are some useful budgeting tips that everyone who wants to buy a home should follow before they do so. How much house can I afford.

1. Make an emergency fund

When you have unexpected costs, your emergency fund is your first line of defense. Believe us, they will come up. Life is full of surprises, like having to fix your car suddenly, getting an unexpected medical bill, or changing jobs. Before you buy a house, experts say you should have three to six months’ worth of living expenses saved up in a liquid account.

Why is this important when figuring out how much house can I afford Because your home shouldn’t put your money at risk. If you don’t have any savings and something goes wrong with your money, you might have trouble making your mortgage payments, which could lead to late fees, penalties, or even foreclosure.

Let’s say your monthly bills, including your future mortgage, add up to $4,000. In that case, your emergency fund should be between $12,000 and $24,000. This cushion makes sure you can deal with short-term problems without using credit cards or personal loans, which only make your debt and stress worse.

If you’re still saving for your down payment, make your emergency fund first. Knowing you have a safety net makes owning a home a lot less stressful. Mortgage Affordability.

2. Take into account hidden costs

Most people only think about their mortgage affordability when they figure out how much house they can afford. But first-time buyers may not be aware of the hidden costs of owning a home. Here are some important things to think about:

Costs of closing: These are the costs you have to pay when you buy something. They usually range from 2% to 5% of the home’s purchase price and include the appraisal fee, property insurance, and the lender’s fee. Closing costs for a $400,000 home can easily be between $8,000 and $20,000.

- Repairs and upkeep: Homeowners are responsible for all upkeep, unlike renters. Experts say that you should set aside 1–2% of the value of your home each year for repairs. That’s about $3,500 to $7,000 a year for a $350,000 home.

- HOA Fees: If you live in a neighborhood with a homeowners association, you pay a monthly or quarterly fee for things like landscaping, amenities, or keeping the neighborhood clean.

- Utilities and upgrades: Bigger homes usually have to pay more for electricity, water, and heating. It might also be a good idea to set aside money for new furniture, appliances, or home improvements.

- These extra costs add up fast. If you don’t include them in your budget, you might end up “home stranded,” which means you own a home but can’t afford to pay for other living costs.

3. Get preapproved, but use your money wisely.

Getting preapproved by a lender will help you figure out how much money you can borrow, but it doesn’t mean you can borrow any amount. Just because a bank tells you that you can afford a $500,000 house doesn’t mean that’s the right amount for you.

When figuring out how much house can I afford, don’t just think about the lender; also think about what makes you comfortable. Ask yourself: Will I still be able to save for a vacation and retirement?

If the property tax goes up, will I still be able to pay the mortgage?

Do I have enough money left over each month for my needs and emergencies?

It’s better to buy something for a little less than the allowed amount and have peace of mind about your money than to max out your loan and feel the strain every month.

4. Make a budget for owning a home

Make a fake homeowner budget that includes the following before you buy:

- Paying the mortgage (interest and principal)

- Taxes on property and insurance

- Fees for the HOA or condo (if any)

- Utilities (water, gas, electricity, and trash)

- Fund for repairs and maintenance

For a few months, keep track of how much you spend to see if your planned housing costs are reasonable. If you need to, change your other costs, like going out to eat, getting a subscription, or shopping. This trial run in the real world will show you if you can really afford the way of life that comes with the price of your dream home. Mortgage Affordability

5. Pay off your debts and don't take out any new ones.

Another strong way to grow Before getting a mortgage, you should pay off your debts to find out how much house you can afford. A lower debt-to-income ratio (DTI) means a better mortgage affordability rate and more buying power.

Don’t use credit cards or loans to pay for big things like cars or new credit cards while you’re buying a home. These can make your DTI go up, your credit score go down, and lenders nervous. Instead, work on paying off your current debts, especially credit cards with high interest rates. This will make your application stronger and give you more money each month.

Budgeting wisely isn’t just something you do before you buy a house; it’s something you do for the rest of your life to make owning a home fun and stress-free. If you plan ahead, save money and stick to your budget, you will find that figuring out ‘How much house can I afford‘ is a fun and rewarding journey.

Regional Differences

One of the most important things to think about when trying to figure out how much house can I afford is where you want to live. Your location affects more than just your daily life and commute; it also has a big impact on how much you pay for housing. Two families with the same income could buy very different homes if they live in a city where housing costs a lot of money or a rural area where housing costs less.

Knowing about differences between regions can help you set realistic goals, plan your budget correctly, and make better long-term financial choices.

1. The cost of living and housing prices

The cost of living is very different in different cities, states, and countries. The biggest part of that change is usually housing. For instance, you could buy a small condo in Los Angeles or New York City for $400,000, but you could buy a big four-bedroom house in Texas, Ohio, or Tennessee for the same amount. Mortgage Affordability

When figuring out how much house I can afford, it’s important to look at the average prices of homes in the area I’m interested in. Based on recent data, this is a rough example:

Areas with high costs: Median home prices in California, New York, Massachusetts, and Washington, D.C. are often more than $700,000.

- Colorado, Florida, and Virginia are mid-range markets. The average price of a home is between $350,000 and $500,000.

- Texas, Ohio, Indiana, and Alabama are all affordable places to live. Prices are usually between $200,000 and $300,000.

- Your buying power changes a lot depending on where you live, even if your income stays the same. Before you make your budget, always look into what is going on in the local market.

2. Costs of property taxes and insurance

The cost of property taxes and homeowners insurance is another regional factor that affects how much house can I afford.

Property taxes can be different in different counties, and sometimes even in the same state. For example, homeowners in New Jersey and Illinois pay some of the highest property taxes (over 2%), while those in Hawaii and Alabama pay much less (less than 0.5%). Mortgage Affordability.

Homeowners insurance also depends on where you live. Areas that are likely to get hurricanes, wildfires, or floods often have higher premiums. Insurance costs are often higher than average in states like Florida, Louisiana, and California. On the other hand, rates in the Midwest may be much lower.

When you compare homes in different areas, be sure to include these yearly costs in your estimate of how much can I afford. A home that costs a little less in a high-tax area might end up costing more overall than a home that costs more in a low-tax area.

3. Climate and Utility Costs

The climate and the condition of the roads and other buildings in an area also affect how much house can I afford. For instance, in the winter, heating costs can be high in northern states that are cold.

- In the summer, air conditioning may make the electricity bill go up in hot southern areas.

- Septic systems, private wells, and propane tanks may be needed in rural areas, and all of these things cost extra to keep up. Mortgage Affordability.

These differences can quickly add a few hundred dollars to the monthly budget. If you’re moving, look up the average costs of utilities and maintenance to get a better idea of how much you can afford.

4. The job market, wages, and the local economy

It’s not just the cost of housing that makes a home affordable; it’s also the potential for income. In a smaller city like Tulsa or Des Moines, a salary of $100,000 is not as high as it is in San Francisco. In big cities, wages are often higher, but so are the costs of living, rent, and taxes.

When figuring out how much house can I afford, think about both sides:

Income Level: How much do people in your area make on average?

Cost of living: How much do groceries, transportation, and healthcare cost in your area? If the cost of living goes up faster than your income, it becomes harder to afford things, even if housing prices stay the same.

Mortgage Affordability

5. How affordable is it in cities, suburbs, and rural areas?

Where you live—city, suburb, or rural area—can also have a big impact on how affordable it is.

- Town centers are easy to get to, walkable, and have a lot of amenities, but property prices per square meter are usually the highest.

- Suburbs: Usually a good mix of things—bigger houses, better schools, and more space for less money.

- Rural areas: housing is often the cheapest, but they may not have good roads, jobs, or services nearby.

- If you want to get the most out of How much house can I afford? Moving just 20 to 30 miles outside of a big city can sometimes double how much you can buy.

6. Differences between countries

If you’re thinking about moving to another country or investing in another country, the cost of living changes even more. For instance, Canada, Australia and the UK have strict rules about lending, and housing costs are high in big cities. Real estate in emerging markets in Asia or Eastern Europe may be cheaper, but they also have different financial systems and risks.

Before buying a home abroad, always check the local laws about mortgages, taxes and currency stability.

Bottom Line

Regional differences can make or break your home-buying strategy. The key is to evaluate not just the price of the home, but the total cost of living in that region — including taxes, utilities, insurance, and income opportunities. Only then will you have a true understanding of How much house can I afford in your chosen location.

Conclusion: Make Your Homeownership Dream a Reality

Buying a house is one of the most exciting things you’ll ever do, but it’s also one of the biggest financial decisions you’ll ever make. When you ask yourself, “How much house can I afford?” you’re not just making a budget; you’re taking a step toward taking control of your money. You’re not just getting ready to buy a house when you take the time to look at your income, debt, savings, credit, and lifestyle. You’re also setting yourself up for long-term financial freedom.

Let’s go over what we talked about:

- You learned what affordability really means. It’s not just about getting a loan; it’s also about keeping your balance and security after you buy.

- You’ve learned how to figure out how much house you can afford based on your income, debt-to-income ratio (DTI), and down payment.

- You’ll learn about the most important things that affect how much you can afford, like credit scores, mortgage affordability, property taxes, loan terms, and insurance.

- You learned how to use tools and calculators to get clear, data-driven information before meeting with a lender.

- You learned how to budget for emergencies, hidden costs, and better money management.

And finally, you know that things like the cost of living, taxes, and income levels in different parts of the country can affect what kind of housing is realistic for you.

You do not just get number when you put all of this information together, you also get clarity. You will feel good about entering the market because you know exactly what fits your budget and long-term goal.

A Smart Homebuyer’s Mindset

Finding the right balance between comfort, stability and sustainability is more important than buying the biggest or most impressive property you can afford. A home that is really affordable lets you.

- Pay off the mortgage without worrying about money

- Keep saving for your goals in the future

- Easily take care of maintenance and fees

- Live the way you want to without feeling limited

Before you make an offer, double-check your math, go over your budget again, and make sure the numbers are in line with what you feel comfortable with. Lenders will look at how much you can afford, but only you know how much you should spend. Mortgage Affordability

If you’ve done your research and set reasonable limits, owning a home will feel like a blessing instead of a burden. You can also try Home Affordability Calculator for every country by knowing there taxes and mortgage Affordability interests.

Next Steps: Take Control of Your Home Affordability Today

You don’t have to go on this trip by yourself. Knowing how much house you can afford is the first step to making smart choices, whether you’re buying your first home or planning your next big move.

Step 1: Use a reliable [online Home affordability calculator] to find out what price range is best for you.

Step 2: Check how healthy your finances are— Look at your credit score, debt-to-income ratio, and emergency fund.

Step 3: Contact a mortgage expert you trust who can help you figure out the best options for you based on your situation. To know your Mortgage Affordability.

Are you ready to find the perfect home that fits your budget? Calculate your Mortgage affordability now with an online tool and take the first step toward owning a home without stress.

Or, if you want expert help: Talk to a mortgage expert today and get a custom report on How Much House Can I Afford that takes into account your real numbers and goals.

Remember that buying a house isn’t just about the house; it’s also about your financial happiness. When you really know how much house can I afford, you’ll not only buy better, but you’ll also live better.

Forex Win Master

Read More About Related Topics

- How Your Credit Score Affects Home Affordability

- What Is a Good Debt-to-Income Ratio for Buying a House?

- Down Payment Guide: How Much Should You Put Down?

- Hidden Costs of Buying a Home You Might Forget

- Renting vs. Buying: Which Can You Actually Afford

- First-Time Homebuyer Budget Checklist

- Mortgage Types Explained: Which One Fits Your Budget?

- Regional Home Affordability Trends in UNITED STATES

- How to Use a House Affordability Calculator (Step-by-Step)